Another draft written over 3 years ago, fun to read these now...

Inflation

I mentioned this briefly in one of my early posts but I would like to expand upon it here. Home prices have tracked general inflation very closely over the course of history. Robert Shiller, economist of Case-Shiller index fame, has done extensive research on this matter. There have been periods in history when real estate prices decoupled from inflation, but over a long enough period of time the relationship has ALWAYS come back in line. The housing bubble caused a massive decoupling that, on a national basis, is well on its way to re-coupling now. From a regional perspective however, there are still very large discrepancies is certain markets. The vacation property market along the Charleston coast is one of those markets. Prices have fallen dramatically from their bubble peaks but would still have to fall more than 50% further on most islands to get back in line with the long term general inflation trend.

How much of the housing inflation in our area has been cause by permanent market factors unrelated to the housing bubble? What proportion of our housing price inflation has been caused by regional preference factors and demographic trends? These are impossible questions to answer with certainty but that will not stop me from speculating!

I am biased toward our area, and will concede that prices here, unlike in many retirement areas in Florida and Arizona, will not revert all the way back to where the general inflation trend says they should be. However, the fact remains that an enormous amount of demand was pulled forward during the bubble and there is not a lot of evidence, if any, that those who have not already bought their second home are in a financial position to do so. The baby boomers are incredibly unprepared for retirement, and are relying heavily on the equity in their primary residences to get them through. Those that are prepared, in large part, already own their 2nd home.

Monday, August 19, 2013

The Mirage, the Anchor, and the Shadow:

I'm Back!!!

This post was written more than 3 years ago and saved in draft mode. I don't remember why I didn't post it. Was I right about "sell now, prices will be lower tomorrow" from the summer of 2010? I think I was, generally speaking. I'll take a closer look and post some updates over the next couple of weeks ... stay tuned!

The Mirage:

Real estate values at the top of the bubble were not real, they were a mirage. Okay, the transactions that took place at those prices were real, but the value wasn’t. It was a very grand illusion that was maintained through the force of what I call the cult of real estate. That cult has dissolved and the illusion has been broken. Valuing a vacation property today outside of rental yield is darn near impossible but it’s the only defensible metric we have. What is the expected *average* gross rental income? What are management fees, taxes, association fees, insurance, maintenance, utilities, etc? Take what’s left over and multiply by 12 and that is your ballpark value. If you insist on paying more that is your prerogative, perhaps you have nothing better to do with your cash and the home is just what you are looking for. Just know that you are paying a premium.

The Anchor:

Real estate values are not sticky, people are. Why? Because of cognitive anchoring and emotional bias. Ask yourself, how sticky were prices when they were going up 10-20-30+% PER YEAR during the bubble? Not sticky at all, completely untethered is more like it.

Tell someone that their home’s value has gone up 1000% over the last 15 years for no other reason than ‘because’ and they will accept it without batting an intellectual eyelash. Their brain will fill in all the why’s and what-fors with only the slightest bit of suggestion. “Real estate values always go up, this area is special, your home is beautiful, they're not making any more land, what a great investment, YOU are a great investor, how smart of you to have bought this home, you deserve the money you've made, you EARNED it, it is yours”. Whether someone tells them or they just tell it to themselves, the unquestioning brain accepts it naturally, as undeniable fact, and it becomes hardwired truth.

Oh, but tell someone their homes value has fallen 50% and watch the brain’s defense mechanisms go into action. Tell them it will fall another 50% from here and they will laugh at you. Even though it JUST happened right in front of everyone’s eyes, their brain will consider it absolutely inconceivable that it could happen again. The sticky brain will not even consider it. 50%, fine, 75%, impossible.

It has gotten to the point where we all understand it was a bubble and values are much lower. But the vast percentage of sellers and real estate professionals have believed that “this is it” at every single point in time. Go back through the blogs and try to find someone who didn’t think it was a great time to buy in 2007, 2008, and 2009. Even though the bubble has burst and everyone knows it, the brain does not easily allow for people to accept that we still have a long way to go to get back to sanity in real estate values on our beaches.

The Shadow:

Again, your home’s value is not sticky, your brain is. Clinging with all its strength the to the things that is WANTS to be true and doing everything in its power to discredit any opposing evidence. This brings us to the shadow, shadow inventory that is. How many owners out there want or need to sell but are convinced by their biases and real estate agents that selling now is selling low, and they should wait for higher prices? Look at all the expired listings since 2006, what happened to these homes? What about all the foreclosed homes that are REO or about to be yet the banks refuse to put them on the market because they don’t want to realize the losses (banks keep these homes on their balance sheets at 100 cents on the dollar until they are sold). What about all the owners who never listed, but who would sell in a minute if they could just get last year’s price? They don’t show up in any statistics. There is no way of knowing how many there are out there. I speculate that the total number of homes in shadow inventory, that has been growing for 4 years now, is absolutely massive, perhaps even bigger than the total number of listings now on the market.

What next?

It is no longer, “buy now or be priced out forever.” It is, “sell now, prices will be lower tomorrow.” And even though this has been true each and every day for over three years now, good luck finding more than a handful of sellers or real estate professionals who have believed it for even one of those days. Their emotional bias’ are just too deep seated to be overcome. As a result, the shadow inventory remains in the shadows and the listed inventory is for the most part obscenely overpriced. The market clearing price is much lower than where current transactions are taking place.

This post was written more than 3 years ago and saved in draft mode. I don't remember why I didn't post it. Was I right about "sell now, prices will be lower tomorrow" from the summer of 2010? I think I was, generally speaking. I'll take a closer look and post some updates over the next couple of weeks ... stay tuned!

The Mirage:

Real estate values at the top of the bubble were not real, they were a mirage. Okay, the transactions that took place at those prices were real, but the value wasn’t. It was a very grand illusion that was maintained through the force of what I call the cult of real estate. That cult has dissolved and the illusion has been broken. Valuing a vacation property today outside of rental yield is darn near impossible but it’s the only defensible metric we have. What is the expected *average* gross rental income? What are management fees, taxes, association fees, insurance, maintenance, utilities, etc? Take what’s left over and multiply by 12 and that is your ballpark value. If you insist on paying more that is your prerogative, perhaps you have nothing better to do with your cash and the home is just what you are looking for. Just know that you are paying a premium.

The Anchor:

Real estate values are not sticky, people are. Why? Because of cognitive anchoring and emotional bias. Ask yourself, how sticky were prices when they were going up 10-20-30+% PER YEAR during the bubble? Not sticky at all, completely untethered is more like it.

Tell someone that their home’s value has gone up 1000% over the last 15 years for no other reason than ‘because’ and they will accept it without batting an intellectual eyelash. Their brain will fill in all the why’s and what-fors with only the slightest bit of suggestion. “Real estate values always go up, this area is special, your home is beautiful, they're not making any more land, what a great investment, YOU are a great investor, how smart of you to have bought this home, you deserve the money you've made, you EARNED it, it is yours”. Whether someone tells them or they just tell it to themselves, the unquestioning brain accepts it naturally, as undeniable fact, and it becomes hardwired truth.

Oh, but tell someone their homes value has fallen 50% and watch the brain’s defense mechanisms go into action. Tell them it will fall another 50% from here and they will laugh at you. Even though it JUST happened right in front of everyone’s eyes, their brain will consider it absolutely inconceivable that it could happen again. The sticky brain will not even consider it. 50%, fine, 75%, impossible.

It has gotten to the point where we all understand it was a bubble and values are much lower. But the vast percentage of sellers and real estate professionals have believed that “this is it” at every single point in time. Go back through the blogs and try to find someone who didn’t think it was a great time to buy in 2007, 2008, and 2009. Even though the bubble has burst and everyone knows it, the brain does not easily allow for people to accept that we still have a long way to go to get back to sanity in real estate values on our beaches.

The Shadow:

Again, your home’s value is not sticky, your brain is. Clinging with all its strength the to the things that is WANTS to be true and doing everything in its power to discredit any opposing evidence. This brings us to the shadow, shadow inventory that is. How many owners out there want or need to sell but are convinced by their biases and real estate agents that selling now is selling low, and they should wait for higher prices? Look at all the expired listings since 2006, what happened to these homes? What about all the foreclosed homes that are REO or about to be yet the banks refuse to put them on the market because they don’t want to realize the losses (banks keep these homes on their balance sheets at 100 cents on the dollar until they are sold). What about all the owners who never listed, but who would sell in a minute if they could just get last year’s price? They don’t show up in any statistics. There is no way of knowing how many there are out there. I speculate that the total number of homes in shadow inventory, that has been growing for 4 years now, is absolutely massive, perhaps even bigger than the total number of listings now on the market.

What next?

It is no longer, “buy now or be priced out forever.” It is, “sell now, prices will be lower tomorrow.” And even though this has been true each and every day for over three years now, good luck finding more than a handful of sellers or real estate professionals who have believed it for even one of those days. Their emotional bias’ are just too deep seated to be overcome. As a result, the shadow inventory remains in the shadows and the listed inventory is for the most part obscenely overpriced. The market clearing price is much lower than where current transactions are taking place.

Monday, July 26, 2010

Overestimating Sepculation?

Wait a minute, you are exaggerating the role of speculation!

I have been accused before of exaggeration the role of speculators in the housing bubble along the 'Charleston Coast'. "Sure there was some speculation and greed" the story goes, "but most of the buyers were your typical wealthy/affluent 2nd home shoppers. Whether it be Wall Street money heading to Kiawah, Charleston executives headed to Edisto, or Big Law Chicago money headed to Folly Beach; the dramatic price gains over the 15 year bubble were just a natural outgrowth of too much demand and not enough supply."

Well, obviously there was too much demand and not enough supply, but why?

Two reasons:

1) Even if none of the demand came from speculative sources, it was greatly influenced by the delusional mentality that real estate prices only go up. The housing bubble didn't get out of hand simply because of the number of buyers, but because of the conventional wisdom that no price was too high to pay. Combine this with almost unlimited access to capital and the real estate market along the South Carolina coast. as well as in many other places, became completely detached from reality. The cult of real estate affected almost everyone, whether you would consider them a legitimate vacation home buyer or simply an opportunist. For the most part, the mentality was the same amongst both groups.

Just because someone is a wealthy retiree, it doesn't mean that paying $1,500,000 for a beachfront home that sold for $300,000 ten years earlier (in an economy running at 2.3% inflation), isn't speculative, not to mention irrational.

2) Real estate is priced, and valued, at the margin.

Let's say there are 10 very similar homes for sale in an area for roughly $300,000 each. Let's say that a bunch of 'well-off vacation home shoppers' and one real estate speculator (Starbucks employee with a brother-in-law who works at Countrywide) come to look at them. What happens when the speculator decides to bid $400,000 for one of the homes? In a rational world all of the other 'shoppers' look at the bidder like he is crazy and the seller rushes through the paperwork before the speculator realizes his mistake. In the housing bubble world all the 'well-off vacation home shoppers' start falling over each other to bid $450,000 on the remaining homes. Why? Because they are certain that real estate prices only go up (their real estate agent told them so after all) and they will double their money in a few short years no matter what price they pay. It only takes a very small number of speculators to push up prices for everyone when a housing bubble mentality exists.

Where to from here?

As illustrated in the previous post, the bubble mentality is gone, and so are the vast majority of speculators. Even when one does pop up to overpay for a home, most people shrug it off and consider the seller lucky. I know I do. Inventory on and off the market is simply massive, and it will take many years and much further price drops to clear it. Sales have picked up a little this year but it hasn't even put a dent in the inventory of most markets. Judging by asking prices, reality still evades most owners trying to sell. I suspect prices will not bottom until that changes.

I have been accused before of exaggeration the role of speculators in the housing bubble along the 'Charleston Coast'. "Sure there was some speculation and greed" the story goes, "but most of the buyers were your typical wealthy/affluent 2nd home shoppers. Whether it be Wall Street money heading to Kiawah, Charleston executives headed to Edisto, or Big Law Chicago money headed to Folly Beach; the dramatic price gains over the 15 year bubble were just a natural outgrowth of too much demand and not enough supply."

Well, obviously there was too much demand and not enough supply, but why?

Two reasons:

1) Even if none of the demand came from speculative sources, it was greatly influenced by the delusional mentality that real estate prices only go up. The housing bubble didn't get out of hand simply because of the number of buyers, but because of the conventional wisdom that no price was too high to pay. Combine this with almost unlimited access to capital and the real estate market along the South Carolina coast. as well as in many other places, became completely detached from reality. The cult of real estate affected almost everyone, whether you would consider them a legitimate vacation home buyer or simply an opportunist. For the most part, the mentality was the same amongst both groups.

Just because someone is a wealthy retiree, it doesn't mean that paying $1,500,000 for a beachfront home that sold for $300,000 ten years earlier (in an economy running at 2.3% inflation), isn't speculative, not to mention irrational.

2) Real estate is priced, and valued, at the margin.

Let's say there are 10 very similar homes for sale in an area for roughly $300,000 each. Let's say that a bunch of 'well-off vacation home shoppers' and one real estate speculator (Starbucks employee with a brother-in-law who works at Countrywide) come to look at them. What happens when the speculator decides to bid $400,000 for one of the homes? In a rational world all of the other 'shoppers' look at the bidder like he is crazy and the seller rushes through the paperwork before the speculator realizes his mistake. In the housing bubble world all the 'well-off vacation home shoppers' start falling over each other to bid $450,000 on the remaining homes. Why? Because they are certain that real estate prices only go up (their real estate agent told them so after all) and they will double their money in a few short years no matter what price they pay. It only takes a very small number of speculators to push up prices for everyone when a housing bubble mentality exists.

Where to from here?

As illustrated in the previous post, the bubble mentality is gone, and so are the vast majority of speculators. Even when one does pop up to overpay for a home, most people shrug it off and consider the seller lucky. I know I do. Inventory on and off the market is simply massive, and it will take many years and much further price drops to clear it. Sales have picked up a little this year but it hasn't even put a dent in the inventory of most markets. Judging by asking prices, reality still evades most owners trying to sell. I suspect prices will not bottom until that changes.

Thursday, July 22, 2010

Waiting For Godot

Who Will the Buyers (and Sellers) of Tomorrow Be?

From Edisto Beach to Dewees Island, there are thousands of beach properties along the coast outside Charleston looking for a new owner. Not to mention an unknowable amount of shadow inventory sitting off the market for the time being, but not forever. Prices have collapsed but only in relation to the bubble peak. When you look further back at what these properties sold for before the bubble, it becomes obvious why we are saddled with years of inventory. We often hear about, almost in a mythological sense, the buyers that the market is in search of. When will they return and start bidding up prices again? Well, first we must understand who these buyers are, then maybe we can answer the first question about when they will return.

The easiest way to learn who these buyers are is to look at who the buyers were during the bubble. I’ll go over each type, generally speaking, and speculate as to what role they will most likely play going forward.

Wealthy/Affluent Vacation Home Shoppers:

They have always been in the market and always will be. However, a tremendous amount of their demand was pulled forward by the housing bubble. If you had the money it became a ‘no-brainer’ to own a 2nd home. How many wealthy people don’t already have their little piece of heaven? If they don’t, why not, and if they didn’t buy into the bubble on the way up what makes us think they will buy into it on the way down? I think it is fair to say that those members of this group who do not already own their vacation home either just aren’t interested or are quite price sensitive. They are the ones picking and choosing over homes now, but only when they are aggressively priced. Demand is and will continue to be sub-par from them until prices fall further, especially if the economy in general remains weak.

Non-Wealthy Vacation Home Shoppers:

Well, they certainly played their part in driving the bubble, with the help of access to some very creative mortgage banking products. But for all intents and purposes, this group no longer exists (with the exception perhaps of the very low end of the market). Those mortgage products are not coming back, not for this group of buyers anyway, and the 'fog a mirror - get a loan' policy of the mortgage industry is gone for at least a generation. As a group they are sitting on a lot of underwater inventory and they will be net sellers for the foreseeable future, eventually through foreclosure and REO.

Professional Developers/Builders:

Another prime suspect in driving the bubble, they sold homes so quickly that it didn't matter what they paid for the next lot or tear-down. But then the bubble popped and all of a sudden it did matter. Although they will always be around the market, demand from this group is only a dim shadow of its former self. The ones who survived the popping of the bubble are only buying in this market at very steep discounts. More so, they are stuck holding a lot of inventory from the bubble years and will be net sellers for the foreseeable future.

Amateur Developers/Builders/Investors:

This is an easy one, like the non-affluent vacation home shopper, for the most part they no longer exist. They only ever existed because of the housing bubble and get-rich-quick mentality that went along with it. Armed with a 'no price is too high to pay' mentality and a bookshelf full of Robert Kiyosaki texts, they played a key role in driving the housing bubble. Obviously, as with the previous two categories, they will be net sellers for the foreseeable future.

Real Estate Professionals:

Raise you hand if you saw an ‘Agent Owned’ tag on a vacation home listing today. It was good while it lasted but the days of real estate agents grabbing properties off the market before the ink was dry on the listing contract are loooong gone. Yet another group that will be a net seller for the foreseeable future.

Professional Investors:

Here is another group that has always been around and always will be. They are generally driven by rental yield and therefore are seen active primarily on the low-end of the price scale, especially in condos. They are the most price sensitive of all potential buyers and will only be active on properties that are aggressively priced. They did not play much of a role in driving the bubble as they are least likely to overpay for property (which is pretty much what you needed to do to be a buyer in the last 10 years).

Anyone still wondering why there are years and years of unsold inventory hanging over the market?

Clearly the pool of potential buyers has been decimated right along with the housing bubble. The mythological buyers we were waiting for at the top of this post are going to stand us up. Of the six groups highlighted above, four virtually no longer exist as potential buyers (in fact, they are now net sellers!). The remaining two groups are, for the most part, price sensitive and not in any hurry. Wealthy/affluent vacation home shoppers are really the only hope for the market. The only way investors will play a major role is if rental inflation really takes off. Perhaps inflation will halt the fall in prices at some point but as I showed in a previous post, housing prices have run hundreds of percentage points ahead of inflation over the course of the bubble. It will take a tremendous amount of inflation to catch up to current price levels.

So instead of exotic-mortgage laden speculators, developers and real estate professionals running over each other to snatch up any and every available property with reckless abandon, it will be retirees, small business owners, and well-to-do executives picking over the cream of the crop at their leisure. This is a broad group that historically was the primary driver of the vacation home market. With the popping of the housing bubble and the delusions that went along with it, this group is back in the drivers seat. But even this pool of buyers will be smaller than it has been in years because of all the demand that was pulled forward. It is going to be a very long haul to clear the massive inventory out there, and much lower prices will be required to do it. Those waiting for the buyers to return are waiting for Godot.

From Edisto Beach to Dewees Island, there are thousands of beach properties along the coast outside Charleston looking for a new owner. Not to mention an unknowable amount of shadow inventory sitting off the market for the time being, but not forever. Prices have collapsed but only in relation to the bubble peak. When you look further back at what these properties sold for before the bubble, it becomes obvious why we are saddled with years of inventory. We often hear about, almost in a mythological sense, the buyers that the market is in search of. When will they return and start bidding up prices again? Well, first we must understand who these buyers are, then maybe we can answer the first question about when they will return.

The easiest way to learn who these buyers are is to look at who the buyers were during the bubble. I’ll go over each type, generally speaking, and speculate as to what role they will most likely play going forward.

Wealthy/Affluent Vacation Home Shoppers:

They have always been in the market and always will be. However, a tremendous amount of their demand was pulled forward by the housing bubble. If you had the money it became a ‘no-brainer’ to own a 2nd home. How many wealthy people don’t already have their little piece of heaven? If they don’t, why not, and if they didn’t buy into the bubble on the way up what makes us think they will buy into it on the way down? I think it is fair to say that those members of this group who do not already own their vacation home either just aren’t interested or are quite price sensitive. They are the ones picking and choosing over homes now, but only when they are aggressively priced. Demand is and will continue to be sub-par from them until prices fall further, especially if the economy in general remains weak.

Non-Wealthy Vacation Home Shoppers:

Well, they certainly played their part in driving the bubble, with the help of access to some very creative mortgage banking products. But for all intents and purposes, this group no longer exists (with the exception perhaps of the very low end of the market). Those mortgage products are not coming back, not for this group of buyers anyway, and the 'fog a mirror - get a loan' policy of the mortgage industry is gone for at least a generation. As a group they are sitting on a lot of underwater inventory and they will be net sellers for the foreseeable future, eventually through foreclosure and REO.

Professional Developers/Builders:

Another prime suspect in driving the bubble, they sold homes so quickly that it didn't matter what they paid for the next lot or tear-down. But then the bubble popped and all of a sudden it did matter. Although they will always be around the market, demand from this group is only a dim shadow of its former self. The ones who survived the popping of the bubble are only buying in this market at very steep discounts. More so, they are stuck holding a lot of inventory from the bubble years and will be net sellers for the foreseeable future.

Amateur Developers/Builders/Investors:

This is an easy one, like the non-affluent vacation home shopper, for the most part they no longer exist. They only ever existed because of the housing bubble and get-rich-quick mentality that went along with it. Armed with a 'no price is too high to pay' mentality and a bookshelf full of Robert Kiyosaki texts, they played a key role in driving the housing bubble. Obviously, as with the previous two categories, they will be net sellers for the foreseeable future.

Real Estate Professionals:

Raise you hand if you saw an ‘Agent Owned’ tag on a vacation home listing today. It was good while it lasted but the days of real estate agents grabbing properties off the market before the ink was dry on the listing contract are loooong gone. Yet another group that will be a net seller for the foreseeable future.

Professional Investors:

Here is another group that has always been around and always will be. They are generally driven by rental yield and therefore are seen active primarily on the low-end of the price scale, especially in condos. They are the most price sensitive of all potential buyers and will only be active on properties that are aggressively priced. They did not play much of a role in driving the bubble as they are least likely to overpay for property (which is pretty much what you needed to do to be a buyer in the last 10 years).

Anyone still wondering why there are years and years of unsold inventory hanging over the market?

Clearly the pool of potential buyers has been decimated right along with the housing bubble. The mythological buyers we were waiting for at the top of this post are going to stand us up. Of the six groups highlighted above, four virtually no longer exist as potential buyers (in fact, they are now net sellers!). The remaining two groups are, for the most part, price sensitive and not in any hurry. Wealthy/affluent vacation home shoppers are really the only hope for the market. The only way investors will play a major role is if rental inflation really takes off. Perhaps inflation will halt the fall in prices at some point but as I showed in a previous post, housing prices have run hundreds of percentage points ahead of inflation over the course of the bubble. It will take a tremendous amount of inflation to catch up to current price levels.

So instead of exotic-mortgage laden speculators, developers and real estate professionals running over each other to snatch up any and every available property with reckless abandon, it will be retirees, small business owners, and well-to-do executives picking over the cream of the crop at their leisure. This is a broad group that historically was the primary driver of the vacation home market. With the popping of the housing bubble and the delusions that went along with it, this group is back in the drivers seat. But even this pool of buyers will be smaller than it has been in years because of all the demand that was pulled forward. It is going to be a very long haul to clear the massive inventory out there, and much lower prices will be required to do it. Those waiting for the buyers to return are waiting for Godot.

Thursday, January 28, 2010

Hope For a Bottom? (Part 2)

How can you know where you're going if you don't know where you've been?

Okay, most everyone knows that real estate prices along the coast of South Carolina exploded higher during the housing bubble. But does the average home shopper ever really stop to think just how much more they are paying than those that came before them?

Here is a quote I read recently, it was printed in the USA Today in July...

"Despite the risk of hurricanes and shifting sands, quarter-acre oceanfront lots sell for up to ... 10 times their value a decade ago.

Okay, most everyone knows that real estate prices along the coast of South Carolina exploded higher during the housing bubble. But does the average home shopper ever really stop to think just how much more they are paying than those that came before them?

Here is a quote I read recently, it was printed in the USA Today in July...

"Despite the risk of hurricanes and shifting sands, quarter-acre oceanfront lots sell for up to ... 10 times their value a decade ago.

Folly Beach as an upscale community is a new image for an island that has long been known as a working-class refuge from fashionable Charleston to the north."

During the bubble, real estate professionals were not shy about promoting the record price increases. But now, with prices in some cases 50% below the levels of 2006/07, you hear far fewer references to the price appreciation of the past. Now, the reference prices quoted are almost always the bubble peak prices. Now, everything is "on sale!"

Is real estate really "on sale"?

Please re-read that quote above from July in the USA Today. Oh, and by the way, that was July 2000! Here is the full piece.

"Despite the risk of hurricanes and shifting sands, quarter-acre oceanfront lots sell for up to $500,000 — 10 times their value a decade ago.

Folly Beach as an upscale community is a new image for an island that has long been known as a working-class refuge from fashionable Charleston to the north."Just think about that for a minute. Frankly I think the numbers are a little off, the appreciation was probably closer to 600-800%, not 1000%, over the course of the 1990's. But let's not quibble over the details. Prices continued higher up through 2006, where beachfront lots topped out in price somewhere in the neighborhood of $1.6-1.8 million. So when you see a listing claiming to be a "steal", ask yourself, compared to when?

The bottom line is this.

The conventional wisdom, that the housing bubble started in 2002/03, is wrong. The housing bubble in South Carolina coastal vacation properties started blowing long before then. Prices paused slightly during the stock market crash of 2000-02, which made it appear that the bubble started afterward, but this is not the case. Credit the price increases of the 1990's to lifestyle change and demographics if you wish. Certainly some of the price increases are due to factors other than the credit bubble and housing mania mentality. However, I would argue that the total price increase we saw from the early 1990's to the mid 2000's was far too extraordinary to be more than remotely explained by fundamental factors.

An illustrative example.

519 W. Ashley: This home just sold last month for $775,000. This is no doubt a significant discount from what it would have fetched a few years ago, and the lowest priced full oceanfront lot sold in a long time. Most would probably consider it a deal, maybe even a steal. I would simply note that it sold in April of 1996 for $299k. Back out the value of the house, which brings in $25-40k a year in rental income according to the listing, and last month's buyer paid a 200%+ premium above the 1996 price. Compare this to 36% for CPI or 50% for the stock market over that same time period. Do you really think this house was on sale?

Perspective is very important when it comes to pricing assets after a bubble. If your mental anchor is the top of the bubble, prices will seem cheap at every rung of the ladder on the way back down. If you look at the big picture over the long term, the enormous supply of unsold homes on the market starts to make a lot of sense. Of course homes aren't selling, they are far more expensive on a real (inflation adjusted) basis than they have ever been, with the exception of the bubble.

So how far back down will prices go?

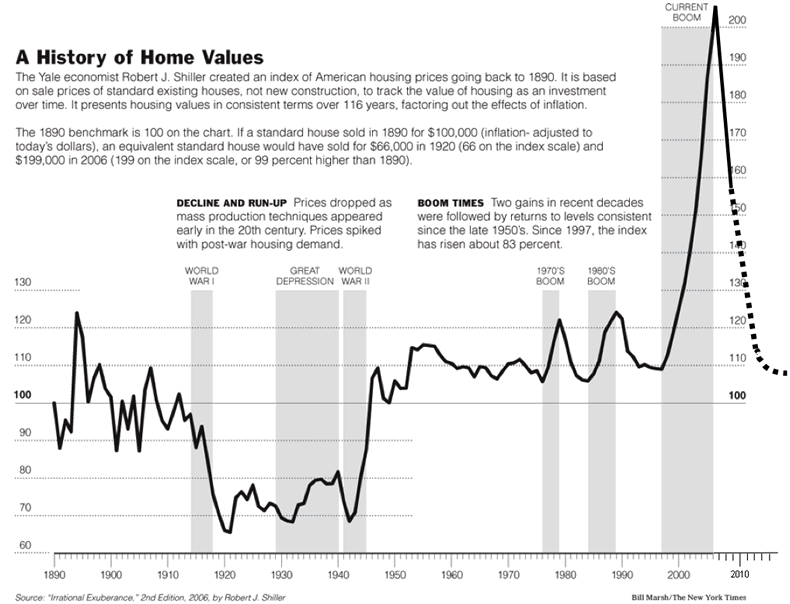

As I've said previously, no one has a crystal ball. But as Robert Shiller has shown, real (inflation adjusted) home prices in the US were little changed for over 100 years before the housing bubble started in the 1990's. In other words, property prices tracked the inflation rate very closely over this long period of time (with obvious ups and downs in between due to the world events shown on the chart). By this yardstick, prices still have a long way to fall.

Continuing to use the beachfront on Folly as our example, from 1993 (post beachfront rebuild by USACE) until 2006 prices on a typical beachfront lot appreciated by over 1000%, approximately 20.5% per year. Or in dollar terms, roughly from $150k (generous) to $1.7 million. The inflation rate as measured by the CPI over that same period of time was 39.5%, or 2.6% per year. I think you can see where I am going with this. Since I believe a certain percentage of the price inflation difference to be structural and permanent (as in: due to non credit/housing mania) over this period, I do not expect a full round trip. I would peg an acceptable property-price inflation rate (for Folly beachfront) at a couple of percentage points above inflation. If we plug 4.6% into the 1993 price level, we get about $322k as a target price for a typical Folly beachfront home site in 2010.

Every year this price target will go up by 4.6%. So another way to look at this target is that prices would have to move sideways from the recent $775k sales price for another 19 years for inflation to catch up. Frankly I think we will land somewhere in between, depending on several factors such as the economy, demographics and the crushing supply of owners out there holding their homes over the market.

Conclusion

Prices went up for so long that people came to believe in a fantasy, that prices would always rise not just in nominal terms but in multiples of the inflation rate as well. Most people still believe in that fantasy, thinking that when the economy recovers it will be back to business as usual with home price appreciation. They are wrong. It was a bubble, and it's not coming back again any time soon.

My conclusion is that, barring a very rapid pickup in the general inflation rate, we are not at the bottom as it concerns nominal property prices on Folly Beach. The same logic applies to all the area islands to varying degrees.

{kind=link}

Continuing to use the beachfront on Folly as our example, from 1993 (post beachfront rebuild by USACE) until 2006 prices on a typical beachfront lot appreciated by over 1000%, approximately 20.5% per year. Or in dollar terms, roughly from $150k (generous) to $1.7 million. The inflation rate as measured by the CPI over that same period of time was 39.5%, or 2.6% per year. I think you can see where I am going with this. Since I believe a certain percentage of the price inflation difference to be structural and permanent (as in: due to non credit/housing mania) over this period, I do not expect a full round trip. I would peg an acceptable property-price inflation rate (for Folly beachfront) at a couple of percentage points above inflation. If we plug 4.6% into the 1993 price level, we get about $322k as a target price for a typical Folly beachfront home site in 2010.

Every year this price target will go up by 4.6%. So another way to look at this target is that prices would have to move sideways from the recent $775k sales price for another 19 years for inflation to catch up. Frankly I think we will land somewhere in between, depending on several factors such as the economy, demographics and the crushing supply of owners out there holding their homes over the market.

Conclusion

Prices went up for so long that people came to believe in a fantasy, that prices would always rise not just in nominal terms but in multiples of the inflation rate as well. Most people still believe in that fantasy, thinking that when the economy recovers it will be back to business as usual with home price appreciation. They are wrong. It was a bubble, and it's not coming back again any time soon.

My conclusion is that, barring a very rapid pickup in the general inflation rate, we are not at the bottom as it concerns nominal property prices on Folly Beach. The same logic applies to all the area islands to varying degrees.

Monday, January 25, 2010

Property of the Week

Keeping with the beachfront theme...

2102 Point Street on Edisto Island

Great Point Street location right on the beach. This home was built in 2005 and has 6 bedrooms and 5.5 baths, about 3200sf. You can view all listing details here. It appears to be a well built home with most of the bells and whistles you would expect.

A little history.

Well, the lot was purchased in early 2005 for $1,075,000 and the buyer didn't waste any time building and selling the new home, which fetched $2,100,000 in September of the same year. The house was sold again in June of 2006 for $2,425,000. The current asking price is $2,475,000, having been reduced from $2,935,000 not too long ago considering how long it's been on the market. Zillow claims one year, but the home was originally listed much earlier than that.

So what should you pay for it?

It is not often these days that a good comparable sale can be identified for a home like this. Especially on Edisto where there has been only one oceanfront sale in the last 1 1/2 years, not including the very poorly elevated lots up towards the campground (which these days have to be reduced below $600k to even have a chance of selling). Fortunately for the comparison shopper, that one sale was the house right next door, 2101 Point Street, which sold last August for $1,450,000!

I know what you are thinking, this must have been an old beach cottage from the 1950's that sold close to lot value. But that is not the case; 2101 Point Street is a 3750sf home built in 2002 with 6 bedrooms and 6.5 baths. It has most of the bells and whistles of its next door neighbor with just a few more years of wear and tear. Here it is...

Looks kind of familiar doesn't it?

This is an easy one, you start with $1,450,000 and work from there. Maybe you think 2102 is much nicer or you think the buyer of 2101 Point St. got a great deal, in which case you should be willing to pay a little more for 2102 Point St. Or maybe you see the extra square footage at 2101 Point St. or you think the buyers overpaid in which case you should look to pay a little less. Either way, I don't see how the difference should be more than 10%.

Also, if you look at the 2006 sale price, $1.45 million would be a discount of 40% from the middle of 2006. This is not out of line with other properties on Edisto. Of course if you're like me you ultimately expect more than a 40% pullback in prices but I'll leave that for another post.

Next week I will try to highlight something a little more down to earth...

2102 Point Street on Edisto Island

Great Point Street location right on the beach. This home was built in 2005 and has 6 bedrooms and 5.5 baths, about 3200sf. You can view all listing details here. It appears to be a well built home with most of the bells and whistles you would expect.

A little history.

Well, the lot was purchased in early 2005 for $1,075,000 and the buyer didn't waste any time building and selling the new home, which fetched $2,100,000 in September of the same year. The house was sold again in June of 2006 for $2,425,000. The current asking price is $2,475,000, having been reduced from $2,935,000 not too long ago considering how long it's been on the market. Zillow claims one year, but the home was originally listed much earlier than that.

So what should you pay for it?

It is not often these days that a good comparable sale can be identified for a home like this. Especially on Edisto where there has been only one oceanfront sale in the last 1 1/2 years, not including the very poorly elevated lots up towards the campground (which these days have to be reduced below $600k to even have a chance of selling). Fortunately for the comparison shopper, that one sale was the house right next door, 2101 Point Street, which sold last August for $1,450,000!

I know what you are thinking, this must have been an old beach cottage from the 1950's that sold close to lot value. But that is not the case; 2101 Point Street is a 3750sf home built in 2002 with 6 bedrooms and 6.5 baths. It has most of the bells and whistles of its next door neighbor with just a few more years of wear and tear. Here it is...

Looks kind of familiar doesn't it?

This is an easy one, you start with $1,450,000 and work from there. Maybe you think 2102 is much nicer or you think the buyer of 2101 Point St. got a great deal, in which case you should be willing to pay a little more for 2102 Point St. Or maybe you see the extra square footage at 2101 Point St. or you think the buyers overpaid in which case you should look to pay a little less. Either way, I don't see how the difference should be more than 10%.

Also, if you look at the 2006 sale price, $1.45 million would be a discount of 40% from the middle of 2006. This is not out of line with other properties on Edisto. Of course if you're like me you ultimately expect more than a 40% pullback in prices but I'll leave that for another post.

Next week I will try to highlight something a little more down to earth...

Friday, January 22, 2010

This is Funny

I just found this website today, related to the house on IOP I blogged about earlier. This is the other $3.5 million house being auctioned on January 30th. Apparently no one wanted to buy it last year for $3 million, if this site is accurate. Maybe they will have more luck at a higher price this year...

Luxury Oceanfront Estate for Sale at Auction near Charleston SC on Saturday March 21, 2009.

Grand South Auctions will be offering the most exquisite Oceanfront Estate located on the Isle Of Palms that sits one of the largest beachfront lots on the island. Newly constructed by award-winning Thomas M. Evans Construction, this 8 bedroom home with 7 full baths and 2 half-baths is like a piece of art.

Recenlty appraised well over $7,000,000 (US Dollars), the minium bid is $3,000,000.

Subscribe to:

Posts (Atom)